Nick Younger, an attorney who went their household members this present year from Phoenix to Evergreen, Texas, has joined so you’re able to book after seeing exactly how aggressive this new homebuying markets try past spring season.

Which have a great homebuying finances anywhere between $one million and you can $1.5 billion, he with his partner remain trying to find one perfect treasure – property which have five bedrooms to expand within the making use of their around three high school students.

These include viewing financial pricing, in addition to other factors, plus inflation, the condition of new savings overall, and presidential election.

There is not a ton of added bonus to find currently, Younger stated before the fresh new Provided statement. But timing the business try a good fool’s errand.

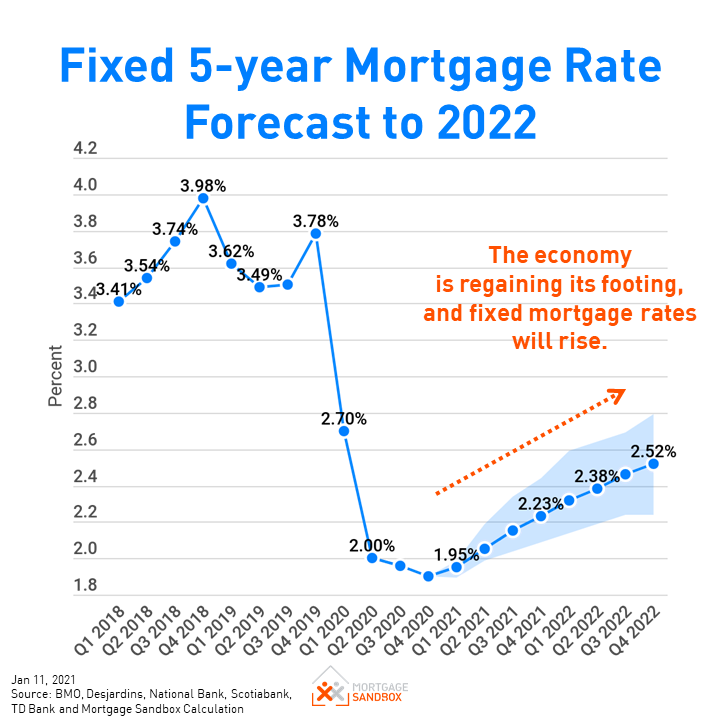

Real estate professionals off Phoenix so you can Tampa, Fl, say of many family customers was looking forward to home loan cost to-fall lower than 6%. Most are in hopes prices can also be go back to the brand new lows regarding around three in years past.

The thing i you will need to would is actually render all of them back to reality, said Mike Opyd, a broker with Re/Max Largest inside Chicago. I let them know, ‘if you happen to be dedicated to to invest in, be in now.

In order to Opyd’s point, the newest pullback when you look at the home loan pricing and a pickup throughout the likewise have out-of house in the market alllow for a good background having house customers that it fall, normally a reduced time of year to have household sales.

Looking forward to prices so you can possibly ease next the following year you’ll hop out consumers against increased battle toward household needed. Meanwhile, potential sellers may still stand lay.

Just remember that , 76% of men and women which have home financing keeps a rate lower than 5%,” said Leo Pareja, President out-of eXp Realty. “Therefore, we possibly may understand the also have-demand instability indeed rating a small worse about near title.

Refinancing spree

When you look at the February, Yae, a compensation specialist, was quoted a great 7% financial price. Once the deal is actually done, his rate had go lower only to in the 6.63%.

I wish to re-finance at 5% otherwise 5.25%, however, I just don’t know if that’s practical and if that’s gonna take more than 24 months to obtain here,” he said.

Yae you certainly will straight down his monthly payment from the more or less $300 thirty day period in the event the he refinances their $407,000 financial to 5.5%.

One to principle to look at when refinancing is whether or not your decrease your existing speed because of the 50 % of to 3-residence out-of a percentage point.

Shortly after people watched list high rates of interest one to peaked about a year ago to 8%, the majority are sales has the benefit of one basically bring buyers an easy method aside of their current price just after it comes down back off while the good answer to quell visitors hesitancy.

Loan providers is increasingly bending with the old big date the rate adage because of the combining amazing financing having refinancing bonuses regarding jump

Its providing a great deal Eagle payday loans online more importance, told you Mike Fratantoni, chief economist on MBA. Delivering closed for the good eight% price forever – for a primary-day customer, it is frightening.”

Navy Federal Borrowing Union told you they started giving its well-known no-refi rates drop inside 2023, which enables buyers to lessen the rate to have good $250 fee while keeping the rest of the terminology toward unique mortgage.

Of numerous homeowners is actually deciding for both new temporary speed buydowns and you will free refinancing, told you Darik Tolnay, department director of CrossCounty Financial into the Lakewood, Colorado.

All of them want a house, therefore if some one turns up with a thought to make it inexpensive, given the standard sentiment, folks are desperate to keeps choices, Tolnay told you.

The new muted frame of mind to own mortgage pricing actually leaves potential customers and you may sellers having a familiar difficulty: Test the new housing market now or wait around to own possibly lower pricing.